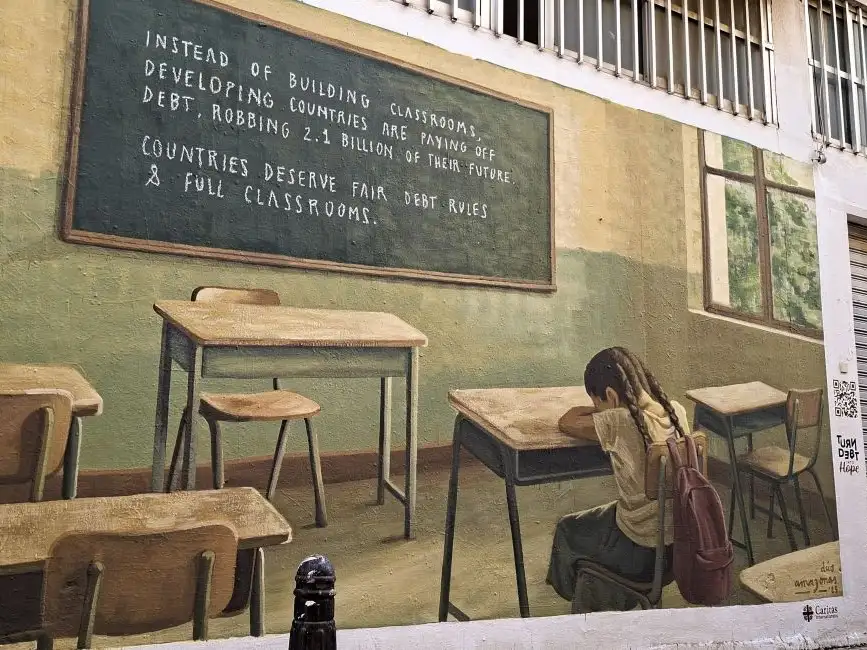

Often, low-income countries have repaid their original debts but they're paying them several times over because of sky-high interest. The current system isn't working. We believe that paying debts should not be put ahead of funding vital public services like health and education. Doing so means debt payments to lenders are being prioritised over life itself.

Private lenders lent to lower income countries at high interest rates – around 6-10% - at a time when they were lending to governments like the US and UK at 0-1%. They supposedly charged these high interest rates because of the risk of not being paid. Therefore, the lenders were always aware that defaulting might be a risk.

Over recent years we have had a succession of shocks – the Covid pandemic, rising food and energy prices, rising global interest rates, and climate disasters. The risk has materialised, and so private lenders must be made to take part in debt relief. Otherwise they will make mass profits, while people in the affected countries will suffer from declining public services and economic stagnation.

Existing structures are not providing solutions to corruption. Only under a more transparent and comprehensive global debt system can corruption be tackled. Developing a transparent global debt registry is one systemic change that would enable citizens to better hold borrowing governments to account.

History demonstrates that, overall, money gained from debt relief is not spent irresponsibly or illegitimately. Indeed, following the Jubilee 2000 campaign, in countries that had debts cancelled children completing primary school increased from 45 per cent to 66 per cent as the money saved on debt repayments went into public services.

More broadly, without global economic structures that enable low-income countries’ economic and political development – including the development of strong political institutions, economic growth, and investment in public services – tackling corruption is extremely difficult. Enabling long-term development by reforming global debt structures is therefore essential to global efforts to reduce corruption.

Not if we reform the system to stop the cycle of debt crises from happening. We need clear legislation and a permanent global debt mechanism to ensure that debts are agreed transparently and that there is a functional relief and restructuring framework.

This will incentivise lenders to be more responsible with their loans, taking greater care over whether they can be repaid. A transparent register of loans would also help hold governments and lenders to account, and so make problem debts less likely to arise.

Beyond this, we need to tackle other underlying causes of lower income countries being so dependent on debt in the first place, such as tax avoidance and evasion, unfair trade rules, and the climate emergency.

CAFOD has campaigned against unjust debt for a long time. After decades of debt justice activism in the Global South, the late 1990s saw the issue of debt become a mainstream issue with the Jubilee 2000 movement.

Between 2000-2015 the global Jubilee campaign won $130 billion of debt cancellation for 36 lower-income countries, which on average reduced their debt by three quarters. In countries that had debts cancelled, children completing primary school increased from 45% in the 1980s-90s to 66% by 2012 as the money governments saved went into public services.

However, the scheme did not prevent debt crises recurring. Despite efforts by the Jubilee 2000 campaign, no new regulations were introduced to make lenders more responsible or transparent. The same structural causes that led to the crisis remain in place. That is why we need action now.

The Bible gives us a model of money lending which is about accompanying the vulnerable in order to help them, rather than to make profits:

“If you lend money to my people, to the poor among you, you shall not deal with them as a creditor; you shall not exact interest from them.” (Exodus 22:25)

Pope Francis spoke repeatedly and clearly about this issue, calling for action in the Jubilee Year:

"I ask that affluent nations acknowledge the gravity of so many of their past decisions and determine to forgive the debts of countries that will never be able to repay them. More than a question of generosity, this is a matter of justice.”